When your loved ones’ future has to be secured, insurance proves to be a mighty instrument. However, sometimes individuals are confused about varying types of policies. Two of the most popular options are term insurance policies and personal accident insurance. They might seem similar at first glance, as both offer financial stability in times of need. However, in actuality, they function in quite dissimilar ways. In order to make the right decision, you need to know how these two policies are different.

What is Term Insurance?

Term insurance policy is the most basic type of life insurance. Here, you pay a premium annually (or monthly) for a specified time period. If you die during that time, your dependents get a lump sum payment, which is referred to as the sum assured. This is used for grocery bills, repayment of loans, children’s education, or some other need.

For instance, if someone purchases a 30-year term insurance policy for ₹1 crore, and they die in the 20th year, the family receives the entire ₹1 crore. However, if they live up to the entire term, there is no payout in the majority of simple term policies.

Briefly, term insurance protects against the risk of death during the policy term.

What is Personal Accident Insurance?

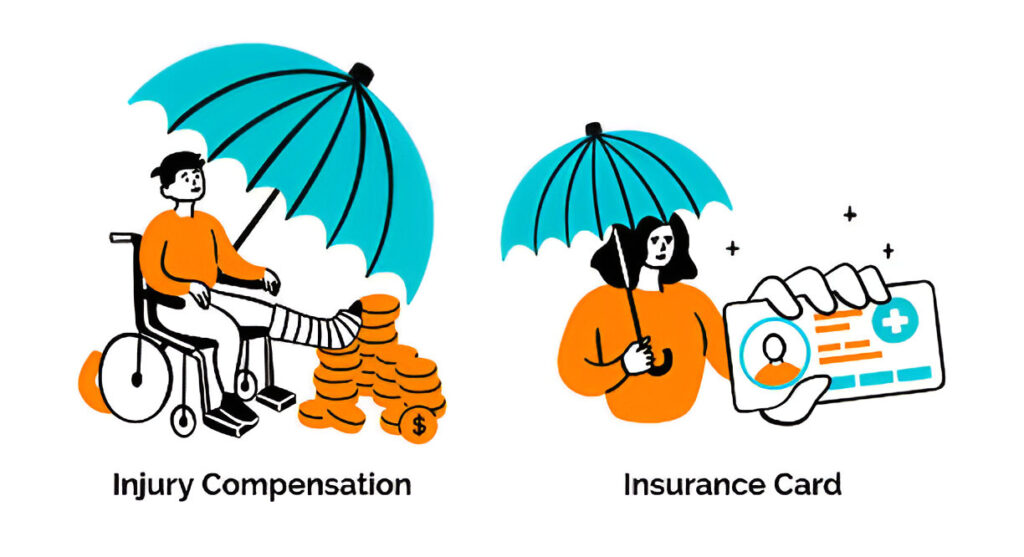

Personal accident insurance, however, cares only about accidents. It protects you if you are the victim of accidental death, disability, or grievous injury due to an accident. It doesn’t cover natural death, illness, or death due to old age.

For example, if an individual is involved in a road accident and ends up dead, the policy pays the family the insured value. Similarly, if the person becomes permanently disabled as a result of injury, he/she can be compensated according to the policy terms.

That is to say, personal accident insurance pays out only if an accident occurs.

The Key Differences

Let us make comparing these two plans easy now.

1. Coverage

- Term Insurance Policy: Insures death by natural causes, disease, or accident.

- Personal Accident Insurance: Insures death or disablement due to an accident only.

2. Purpose

- Term Insurance: Gives total financial protection to your family when you are no more.

- Personal Accident Insurance: Assists if an accident turns your life upside down.

3. Benefits

- Term Income Insurance: Massive compensation (sum assured) to your family if you pass away untimely within the policy duration.

- Personal Accident Insurance: Protection against accidental death, loss of a limb (partial disability), or permanent disability.

4. Premiums

- Term Insurance: Premiums change with age, health, lifestyle, and sum assured. Typically higher than accident policies.

- Personal Accident Insurance: Premiums are considerably lower as the protection is limited to accidents only.

5. Long-Term Security

- Term Insurance: Provides for your family’s financial security regardless of any event of death.

- Personal Accident Insurance: Useful only in the event of an accident, not natural disasters or disease.

Do You Need Both?

It is a frequent question. The fact still stands that both are required individually.

- Term insurance policy is a must for anyone with dependents. It provides your family with funds to survive even in the event of your death.

- Personal accident insurance can be likened to a rider. As accidents are sudden and unforeseen in nature, this policy provides additional coverage in the event of an accident.

Both these policies combined make your financial safety net strong. Consider term insurance as the first pillar of strength, and accident insurance as the second cover.

Real-Life Example

Let us assume that there are two friends – Ravi and Arjun.

- Ravi purchases personal accident coverage worth only ₹50 lakh. He believes it is sufficient. Unfortunately, he has a heart attack and dies. As it was not an accident, nothing goes to his family. They are hardly able to afford the bills.

- Arjun purchases a term insurance policy of ₹1 crore and an accident insurance policy of ₹25 lakh. He is involved in a road accident after a few years and dies. His family gets ₹1 crore under the term policy and ₹25 lakh under accident insurance. Together, they get ₹1.25 crore and become financially stable.

This is the hint towards why it is so vital to comprehend the difference.

Which One to Purchase First?

In case you are beginning from zero, always purchase a term insurance policy first. It insures in most scenarios and protects your family. Then, only if you can afford it, take a personal accident insurance plan for additional security.

Common Myths Disproved

Myth: Accident insurance is sufficient.

Fact: It only covers accidents and not illness or natural death.

Myth: Term insurance is expensive.

Fact: Actually one of the lowest-cost methods of obtaining high coverage.

Myth: Young individuals do not need term insurance.

Fact: The younger you are when you purchase, the lower your premium for the entire term.

Myth: The two policies are the same.

Fact: They are written to cover different purposes and are not interchangeable.

How to Choose the Right Policy

While selecting insurance, remember these:

- Your family requirements: Consider loans, children’s education, and lifestyle costs.

- Your budget: Select coverage which you can pay for in the long run.

- Claim settlement ratio: Always opt for companies having high claim settlement ratio.

- Add-ons: Term insurance policies also provide add-ons like accidental death cover, critical illness, etc.

Conclusion

Personal accident insurance and term insurance have different applications in financial protection. Term insurance is a must for all because it provides coverage against death from any cause, so your family remains secure. Personal accident insurance is an extra protection option, particularly in today’s times with all the road accidents and occupational hazards one puts oneself at risk for.

The intelligent approach is as follows:

- Begin with a good term insurance policy.

- Add cover for personal accidents for added protection.

In this manner, you are completely insured against the uncertainty of life. Bear in mind that insurance is not all about money, it’s about providing your loved ones with a sense of security and confidence for the long term.